The Electronic Money Institution (EMI) license in Finland has established itself as one of the most robust and prestigious fintech authorizations within the European Union. Regulated by the FIN-FSA, this license represents a strategic gateway for tokenization projects, neobanks, and, in particular, stablecoin issuers under the framework of MiCA.

What Does an EMI License in Finland Allow?

Obtaining an EMI license in Finland enables a broad range of operations across the European Economic Area (EEA). Its core capabilities include:

– Electronic money issuance: allows the creation and management of e-money, which under MiCA directly translates into the ability to issue Electronic Money Tokens (EMTs), i.e., fiat-referenced stablecoins.

– Payment services: enables payment accounts, digital wallets, fund transfers, and transactional services.

– Neobank operations: provides the regulatory framework to build and operate a fully digital bank.

– European passporting: once authorized in Finland, the entity can operate across all EU Member States without requiring additional licenses.

Key Context: MiCA and the Central Role of EMI Licenses

With the entry into force of MiCA, the European regulatory architecture clearly separates crypto-asset service providers (CASPs) from stablecoin issuers.

To issue Electronic Money Tokens (EMTs), a CASP license is not sufficient. An EMI license is mandatory. This places EMI institutions at the core of the regulated stablecoin economy in Europe.

Structurally, MiCA does not create a new category for EMT issuers; instead, it anchors them within the existing electronic money framework. This effectively integrates stablecoins into the traditional European financial system.

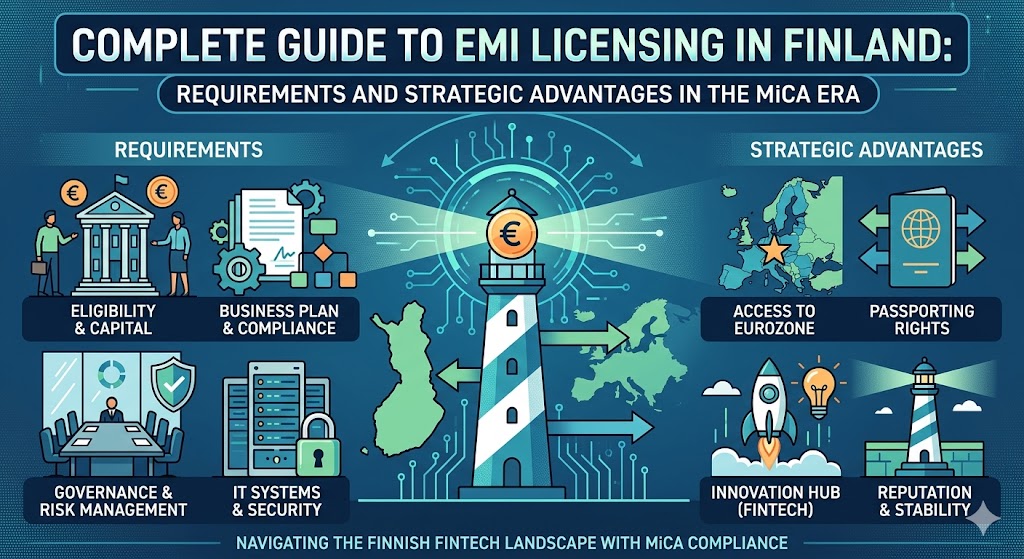

Key Requirements for an EMI License

The application process is demanding and focuses on three pillars: capital, structure, and compliance.

Capital and Regulatory Thresholds

– Minimum initial capital: €350,000

– E-money issuance threshold: €5 million

Exceeding this threshold requires a full EMI license. Below it, a simplified registration regime may apply, though with significant operational limitations.

Additionally, institutions must maintain own funds equivalent to approximately 2% of the total issued e-money, ensuring ongoing financial stability.

Structure, Substance, and Compliance

The FIN-FSA requires real operational substance:

– Company incorporated in Finland

– Physical office (no “letterbox” entities)

– Management team meeting fit & proper requirements

– Full transparency of ownership structure

Compliance requirements include:

– Robust AML/KYC procedures

– Risk management systems

– Safeguarding of client funds

– Secure and auditable IT infrastructure

Key Documentation

– Business plan (3–5 years)

– Operational flow descriptions

– Internal policies (compliance, risk, IT)

– Identification of shareholders and management

Authorization Process Before the FIN-FSA

The process is structured and technical, typically taking between 9 and 12 months:

Phase 1: Preparation

Drafting all legal, financial, and compliance documentation

Phase 2: Formal application

Submission to the FIN-FSA (application fee approx. €6,200)

Phase 3: Technical review

Ongoing interaction with the regulator, including clarifications and additional requests

Phase 4: Authorization

Final approval following a positive assessment

Strategic Advantages

Choosing Finland is not just about compliance—it is about positioning:

– Top-tier EU jurisdiction with strong institutional credibility

– Easier access to banking relationships

– Direct access to payment infrastructure such as SEPA and SWIFT

– Predictable and rigorous regulator

– Ideal framework for Web3 and institutional-grade digital finance

Comparison with Other Jurisdictions

vs. Estonia:

Finland offers stronger institutional credibility, particularly in the post-MiCA regulatory environment.

vs. Lithuania:

Lithuania is faster and more “fintech-friendly,” but Finland provides greater regulatory robustness, which is critical for large-scale and institutional projects.

The Role of BACS in This New Environment

In this evolving landscape where law and technology converge, BACS (Blockchain Arbitration & Commerce Society) introduces an additional legal layer.

Its approach goes beyond licensing support, integrating:

– Legal structuring for Web3 projects

– Advanced compliance design

– Blockchain-adapted dispute resolution systems

– Dual enforcement mechanisms: off-chain (traditional law) and on-chain (code execution)

The combination of a regulated EMI structure with embedded dispute resolution mechanisms enables the creation of financial infrastructures with real legal certainty—not merely formal compliance.

Case Study: Membrane Finance and EUROe

A leading example of the Finnish EMI model is Membrane Finance, issuer of the EUROe stablecoin.

Operating as a licensed EMI in Finland, it has passported its services across the EU and aligns fully with the EMT issuer model under MiCA.

This demonstrates that Finland is not just a theoretical option but a proven jurisdiction for regulated digital asset issuance.

Conclusion

The Finnish EMI license is not a shortcut—it is a strategic commitment.

It is demanding, but it offers:

– Institutional credibility

– Full access to the European market

– Integration with the financial system

– A solid legal foundation for stablecoins and digital payments

For ambitious projects—particularly EMT issuers, neobanks, and Web3 infrastructures—it stands as one of the most robust regulatory options globally.

In this context, having a properly designed legal and compliance architecture from the outset, as promoted by BACS, is not optional—it is a critical factor for scalability and long-term resilience.