Real estate tokenization is often presented as a technological innovation. In reality, it involves something even more profound: a redesign of the legal architecture. And one of the most revealing aspects of this transformation is that many real estate tokenization projects in the U.S. are not structured purely within the United States. Instead, they rely on holding entities in the Cayman Islands.

This is no accident. It reflects a structural shift in how assets, law, and markets interact within the emerging “Internet jurisdiction.”

The Three-Layer Structure: Separating the Asset from Its Digital Logic

The key to understanding this lies in the separation of layers. A typical tokenization structure today operates on three distinct planes, creating an architecture that optimizes each function within the most suitable jurisdiction.

1. The Real Asset (Physical Layer)

The property itself, located in the United States and generally held through a local LLC in jurisdictions such as Texas, Delaware, or Florida. This is where the tangible value resides and U.S. real estate laws apply.

2. The Legal Vehicle (Protective Layer)

A Special Purpose Vehicle (SPV), typically the LLC itself, which isolates the asset and structures legal ownership, protecting it from other liabilities and simplifying management.

It should be noted that this layer presents many tax issues for non-U.S. residents. The U.S. tax system penalizes direct ownership of real estate by foreigners at three critical points.

First, upon receipt of rental payments, which qualify as FDAP (Fixed, Determinable, Annual, or Periodical) income under IRC §1441/1442, subject to a 30% withholding on gross income, without deducting maintenance expenses, mortgage payments, or anything else. A Spanish investor who receives $100,000 annually in rent payments will, in principle, have $30,000 withheld directly by the payer. There is a partial workaround, such as the election under IRC §871(d), which allows the income to be treated as effectively connected income (ECI) from a trade or business in the U.S. With this election, the net income is taxed at progressive rates, but it requires filing an annual U.S. tax return (Form 1040-NR or 1120-F). Operationally, this entails ongoing compliance (1).

Second, at the time of the property sale, the Foreign Investment in Real Property Tax Act (FIRPTA) imposes a 15% withholding tax on the gross transaction price—not on the profit, but on the total amount. If a European fund sells a property worth USD 1 million at a loss, the buyer will still withhold USD 150,000. For any institutional investor, this is unmanageable from a liquidity standpoint.

And finally, upon death, the famous U.S. “Estate Tax” will apply. As the federal tax authority (Internal Revenue Service, 2026) (2) warns, the code establishes a minuscule exemption of just $60,000 for non-resident investors on assets located in the U.S. This represents a stark disparity compared to the exemption (which exceeds $13 million) applicable to U.S. citizens. All capital exceeding that $60,000 threshold is subject to a progressive tax rate that quickly reaches 40%.

To gauge the impact, for example, a $2 million property owned by an Argentine, Mexican, or Spanish investor will generate a tax liability exceeding $700,000 at the time of succession. This level of asset exposure, which is almost confiscatory in nature, rarely appears in the commercial pitch decks of tokenization platforms, but it is, strictly speaking, the true structural driver that justifies the design of the entire offshore legal framework.

3. The Blocker (Tax Layer)

Between the SPV and the foreign holding company, there is often an additional layer that tokenization analyses tend to overlook: a U.S. C Corporation, known as a “blocker corp.”

Its function is precise. By interposing a C Corp between the LLC holding the asset and the offshore issuing entity, foreign investors no longer have direct exposure to a U.S. Real Property Interest (USRPI), thereby efficiently addressing all the tax issues mentioned above. Shares in a C Corp are not a U.S. situs asset for Estate Tax purposes, and exposure to FIRPTA is shifted to the corporate level, where it can be managed with greater operational and tax control. In this way, token holders own, through economic rights, a Cayman Islands entity that, in turn, is a shareholder of a U.S. corporation, which manages the various LLCs and properties.

The trade-off is real: there is corporate double taxation, and the structure adds compliance costs. The decision to include the blocker depends on the capital profile; for pools with a majority of non-U.S. persons, it is almost always the right choice. For structures with predominantly U.S. investors, it may be unnecessary.

4. The Tokenization Layer (Logical Layer)

A holding company, often incorporated in the Cayman Islands, that issues the tokens. These tokens represent economic rights to the underlying structure, not direct ownership of the property.

In most cases, investors do not directly acquire the U.S. property. They acquire tokens linked to the offshore holding entity, which in turn controls or is economically linked to the U.S. SPV. This distinction is subtle but fundamental. Ownership is no longer tied solely to property registration systems; it is mediated by a programmable legal wrapper.

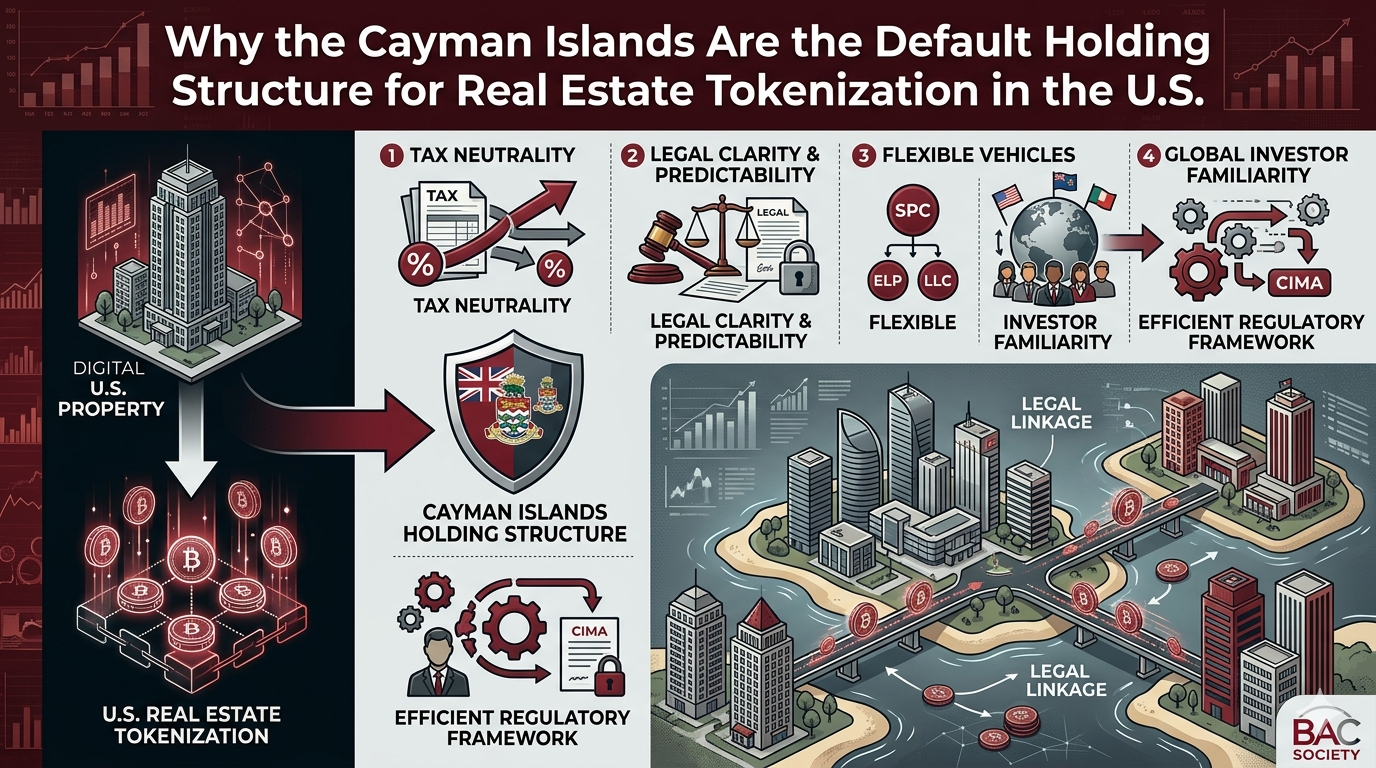

Why the Cayman Islands? The Four Key Factors Behind Their Appeal

The answer is not simply tax efficiency, although that plays a role. The Cayman Islands function as a form of global legal infrastructure. Their advantages can be summarized in four pillars:

Regulatory Neutrality

While the regulatory landscape at the SEC in the U.S. has shifted significantly, particularly following the latest joint ruling by the SEC and CFTC on March 17, 2026 (3). This resolution clearly establishes that tokenization does not alter the legal nature of the underlying asset. A token representing economic rights to real estate, with an expected return derived from third-party management, falls under the category of “digital security.” While this adds legal certainty, the regulatory framework is not yet fully defined.

In contrast, the Cayman Islands offer a much clearer regulatory framework for tokenization. The Virtual Asset Service Providers Act (VASP Act) (4), in effect since 2020 and updated in 2024, establishes a licensing regime administered by the Cayman Islands Monetary Authority (CIMA) that explicitly distinguishes between utility tokens, security tokens, and virtual assets, with registration obligations proportional to the type of issuance. Exempted Companies may issue tokens representing economic rights to underlying assets under a framework that the issuer can know in advance.

Corporate Flexibility

Entities such as “exempted companies” allow for highly customizable governance, which is essential for systems where voting rights and profit distribution are encoded in smart contracts.

Tax Neutrality

The absence of corporate income tax, capital gains tax, or withholding taxes at the entity level makes it an efficient hub for international investors.

Institutional Familiarity

It is not an exotic location. It is an established jurisdiction for investment funds and private equity. The legal ecosystem already exists and is now adapting to tokenization.

In this sense, the Cayman Islands are not a loophole. They are a bridge.

The contrast: why the logic of tokenization is shifting

The limitations of the U.S. system become clearer when viewed in contrast. The United States remains one of the most attractive environments for real estate investment itself. Property rights are robust, markets are deep, and financing is accessible. But when it comes to the token layer, the regulatory landscape is fragmented and often reactive. The equation is different, and recent regulatory developments illustrate this precisely.

The March 2026 joint SEC-CFTC interpretation brought taxonomic clarity: tokens representing economic rights in real estate are digital securities. That did not reduce the regulatory burden; it confirmed it and made it more explicit. Structuring a real estate token offering within the U.S. today entails full compliance with the Securities Act (registration or exemption via Reg D, Reg S, or Reg A+), regulatory differences between states, disclosure costs, transfer restrictions, and a secondary market that remains very limited for domestic security tokens.

The result remains the same: while the asset remains subject to U.S. law, the structure of the issuance shifts overseas. Not because there is ambiguity, but precisely because there is no longer any. Once it is confirmed that the token is a digital security, issuing through an exempted company in the Cayman Islands under Regulation S (targeting exclusively non-U.S. persons) is the path that combines legal certainty, operational efficiency, and access to global capital without the friction of the U.S. domestic market. The hybrid structure is not an anomaly; it is the rational response to a regulatory framework that already knows what it means, but which remains costly to satisfy from within.

The conceptual shift: from contracts to code

But the most important shift is not geographical. It is conceptual. In traditional finance, legal rights are defined in contracts and enforced through the courts. In tokenized systems, part of that legal logic is embedded directly in the code. Tokens do not merely represent ownership; they encode rules about how that ownership behaves: how revenues are distributed, how decisions are made, how transfers occur.

This begins to resemble a new form of lex mercatoria: a body of rules that emerges from market practice rather than state legislation, but is now implemented through digital infrastructure.

The Challenge of Enforcement and Inherent Risks

This evolution raises a critical question: enforcement. If the economic logic of the asset is governed by tokens and smart contracts, what happens in the event of a dispute? What if there is a mismatch between the on-chain representation and the legal reality off-chain? Current structures often rely on traditional legal systems for final enforcement, creating a gap.

-Cross-border regulatory exposure: U.S. authorities may still assert jurisdiction over offshore offerings targeting U.S. investors.

-Governance: Poor design can lead to conflicts between token holders and administrators.

-AML/KYC compliance: Obligations must be carefully managed across all jurisdictions.

Despite these challenges, the direction of the journey is clear. Real estate tokenization is not developing within a single jurisdiction. It is emerging across jurisdictions. The asset, the legal vehicle, and the token layer are increasingly distributed across different legal systems, each chosen for its specific advantages.

Within this architecture, the Cayman Islands have become a central hub—not as an end destination, but as an enabling layer in a broader transformation. What we are witnessing is not merely the digitization of real estate. It is the gradual construction of a new legal geography, where the most important question is no longer “Where is the asset located?” but “Where does its logic reside?”

And increasingly, that logic is shifting toward the Internet infrastructure.

(1) Internal Revenue Service. (9. Februar 2026). Feste, bestimmbare, jährliche oder periodische Einkünfte (FDAP). https://www.irs.gov/individuals/international-taxpayers/fixed-determinable-annual-or-periodical-fdap-income

(2) Internal Revenue Service. (2026). Estate tax for nonresidents not citizens of the United States. https://www.irs.gov/businesses/small-businesses-self-employed/estate-tax-for-nonresidents-not-citizens-of-the-united-states

(3) Commodity Futures Trading Commission. (2026, 17 de marzo). CFTC joins SEC to clarify the application of federal securities laws to crypto assets.https://www.cftc.gov/PressRoom/PressReleases/9198-26

(4) Government of the Cayman Islands. (2024). Virtual Assets Law (2024 Revision). Cayman Islands Monetary Authority. https://www.cima.ky/upimages/lawsregulations/VirtualAssetServiceProvidersAct2024Revision_1716397271.pdf