Crypto taxation enters a new phase of control

Cryptocurrency taxation in Spain is no longer a grey area. With the 2025 Income Tax campaign, the Agencia Tributaria has introduced new specific obligations that confirm a clear shift: the crypto ecosystem is now fully integrated into the tax system.

This evolution is not accidental. It reflects a broader structural transformation: digital assets have moved from being a purely technological niche to becoming a significant component of the wealth of thousands of taxpayers. Bitcoin, stablecoins, DeFi tokens, and other digital assets are no longer marginal—they are part of real balance sheets.

As a result, the Spanish tax framework is evolving accordingly. What we now see is a system that is more demanding in terms of compliance, but also more defined in terms of rules and expectations. Legal uncertainty is being replaced by regulatory clarity—at the cost of increased reporting obligations.

New obligations: more detail, more traceability

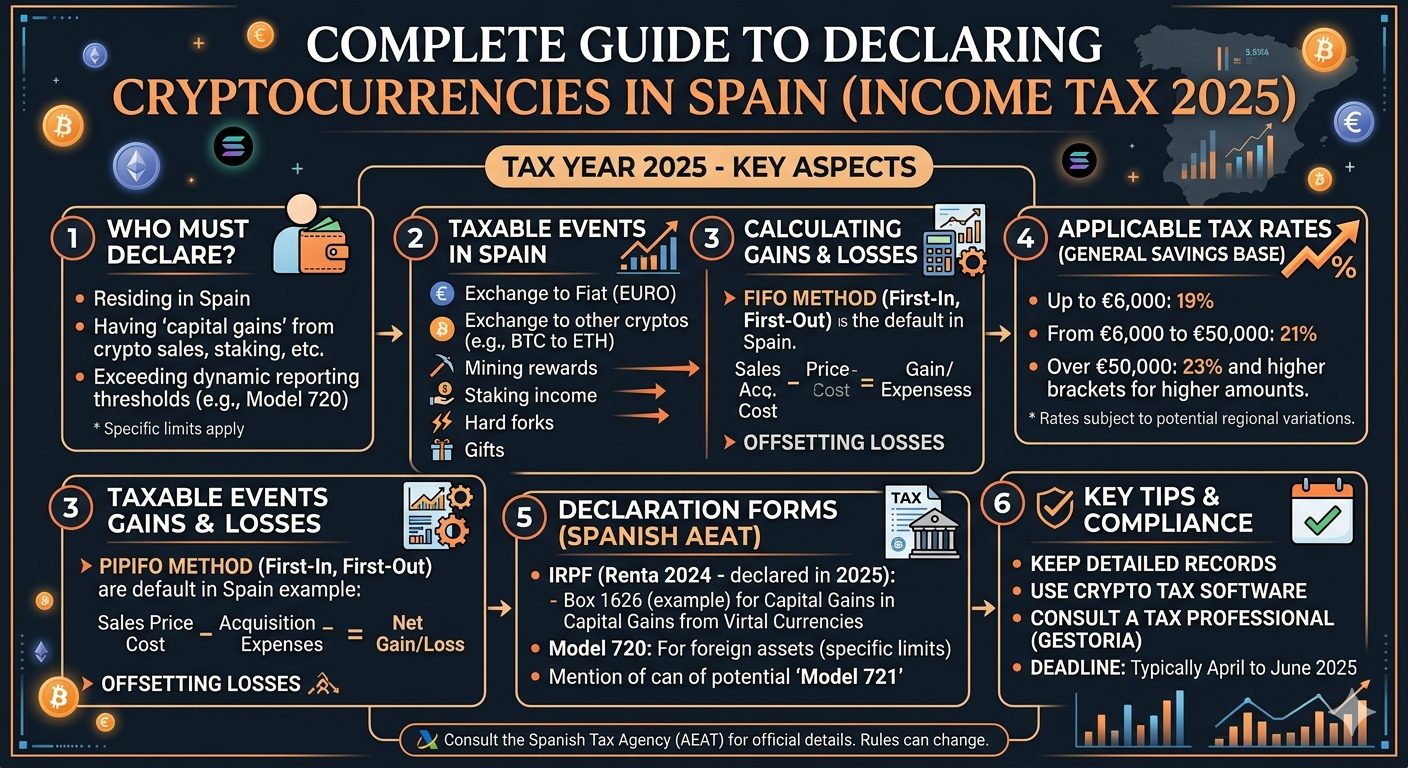

The main novelty for the 2025 tax year is the incorporation of specific reporting fields for cryptocurrencies within the personal income tax return (IRPF).

This change has significant practical consequences:

- It is no longer sufficient to declare a single net gain or loss

- Each individual transaction must be disclosed

- Taxpayers must report dates of acquisition and disposal

- Acquisition and transfer values must be accurately calculated and documented

In practice, this means that the tax authority is requiring a full reconstruction of the taxpayer’s crypto activity over the fiscal year.

This represents a structural shift in the logic of taxation. Previously, crypto reporting could operate under a simplified declarative approach. Now, the system is clearly moving toward full traceability, where each movement of value must be documented and justified.

For many taxpayers, this is the most complex aspect of compliance—not the tax itself, but the operational burden of tracking and organizing historical transactions across multiple platforms and wallets.

The critical point: every transaction is taxable

One of the most persistent misunderstandings in crypto taxation is the belief that taxes are only triggered when cryptocurrencies are converted into euros.

This assumption is incorrect under Spanish tax law.

In Spain, any exchange of one cryptocurrency for another is considered a taxable event that generates a capital gain or loss. This means that taxation arises even if no fiat currency is involved.

Examples include:

-

- Swapping BTC for ETH → taxable event

- Swapping USDT for SOL → taxable event

- Using cryptocurrency to pay for goods or services → taxable event

Each of these operations must be individually assessed to determine whether a gain or loss has occurred, based on the difference between acquisition value and market value at the time of the transaction.

This creates a highly granular tax framework, where even active traders with hundreds or thousands of transactions must compute results on an operation-by-operation basis.

FIFO method: how the tax authority calculates gains

The Agencia Tributaria applies the FIFO (First In, First Out) method to determine which assets are deemed sold.

Under this method:

- The first cryptocurrencies acquired are considered the first to be disposed of

- Gains or losses are calculated based on this chronological order

This methodology can produce significant differences in tax outcomes, particularly in volatile markets or in portfolios where assets have been acquired at different price levels over time.

For example, if a taxpayer bought Bitcoin at multiple price points and later sells part of their holdings, the FIFO method may result in higher taxable gains if the earliest acquisitions were made at lower prices.

Understanding how FIFO applies is essential for accurate tax reporting and for anticipating the tax impact of future transactions.

Tax rates in 2025

Capital gains derived from cryptocurrencies are taxed under the savings income tax base in Spain.

The applicable tax rates for 2025 are:

- 19% up to €6,000

- 21% from €6,001 to €50,000

- 23% up to €200,000

- 27% up to €300,000

- 30% above €300,000

These rates align crypto taxation with other financial assets such as stocks or investment funds. However, the complexity of calculating the taxable base in crypto cases is significantly higher due to the volume and nature of transactions.

Staking and mining: not all income is capital gains

Not all crypto-related income is treated as capital gains. The tax treatment depends on the nature of the activity, and proper legal classification is critical.

Staking

- May be classified as investment income (capital income)

- Particularly relevant in delegated staking models

- Taxation occurs upon receipt of rewards

Mining

- Considered an economic activity

- Taxed under the general income tax base (which can reach approximately 47%)

- May require registration as self-employed (autónomo)

- Entails additional obligations such as accounting and VAT considerations

The distinction between these categories is essential, as it directly impacts both the applicable tax rate and the compliance obligations.

Foreign-held assets: Form 721

One of the most sensitive developments in recent years is the obligation to declare crypto assets held on foreign platforms.

Form 721 requires taxpayers to report:

- Cryptocurrency balances held on exchanges located outside Spain

- When the total value exceeds €50,000

This obligation introduces a new layer of international transparency and aligns crypto reporting with other foreign asset disclosure regimes.

For taxpayers using global exchanges, custodial services, or offshore structures, this requirement significantly increases the level of scrutiny and the risk associated with non-disclosure.

The real shift: from anonymity to full control

Beyond the technical aspects of compliance, the real transformation is conceptual.

The Spanish tax system is evolving toward:

- Full transparency of digital asset holdings

- Enhanced monitoring capabilities

- Integration of blockchain-based assets into traditional fiscal structures

The early perception of cryptocurrencies as anonymous or outside the reach of tax authorities is no longer sustainable.

Today, blockchain analytics, exchange reporting obligations, and international cooperation mechanisms are converging to create an environment of near-total visibility.

Risks of non-compliance

Failure to comply with crypto tax obligations can lead to serious consequences:

- Financial penalties and surcharges

- Retroactive tax reassessments

- Complex and potentially lengthy tax audits

In many cases, the issue is not intentional non-compliance, but the technical difficulty of reconstructing historical transactions, especially for users who have operated across multiple exchanges, wallets, and DeFi protocols.

This complexity increases the importance of proper record-keeping and professional advice.

Strategic opportunity: crypto tax planning

While the new framework imposes stricter obligations, it also creates strategic opportunities for taxpayers who approach it correctly.

Effective tax planning can allow individuals and companies to:

- Optimize their overall tax burden

- Offset gains with losses

- Structure transactions in a tax-efficient manner

- Plan international operations and residency

Crypto taxation is no longer just a compliance issue—it is becoming a strategic area of financial and legal planning.

This is precisely where specialized advisory services provide significant added value.

Conclusion

Cryptocurrency taxation in Spain has entered a phase of maturity and consolidation.

The system is no longer ambiguous or loosely enforced. Instead, it is structured, increasingly sophisticated, and fully integrated into the broader legal and fiscal framework.

In this new environment, the key question is no longer whether crypto activities must be declared.

The real question is how to do so correctly, efficiently, and strategically.