“The prospect of a rapid adoption of dollar-based stablecoins in European tokenized markets is a legitimate concern, as it risks entrenching dependence on the dollar at the very level of settlement infrastructure.”

— Christine Lagarde, President of the European Central Bank, May 2026.

With this statement, Christine Lagarde has publicly acknowledged one of the most relevant monetary phenomena of our time: dollar stablecoins may become the dominant monetary infrastructure of the European digital economy.

The ECB’s concern is understandable. However, the strategy currently being articulated by the European Union may become a strategic mistake of enormous proportions.

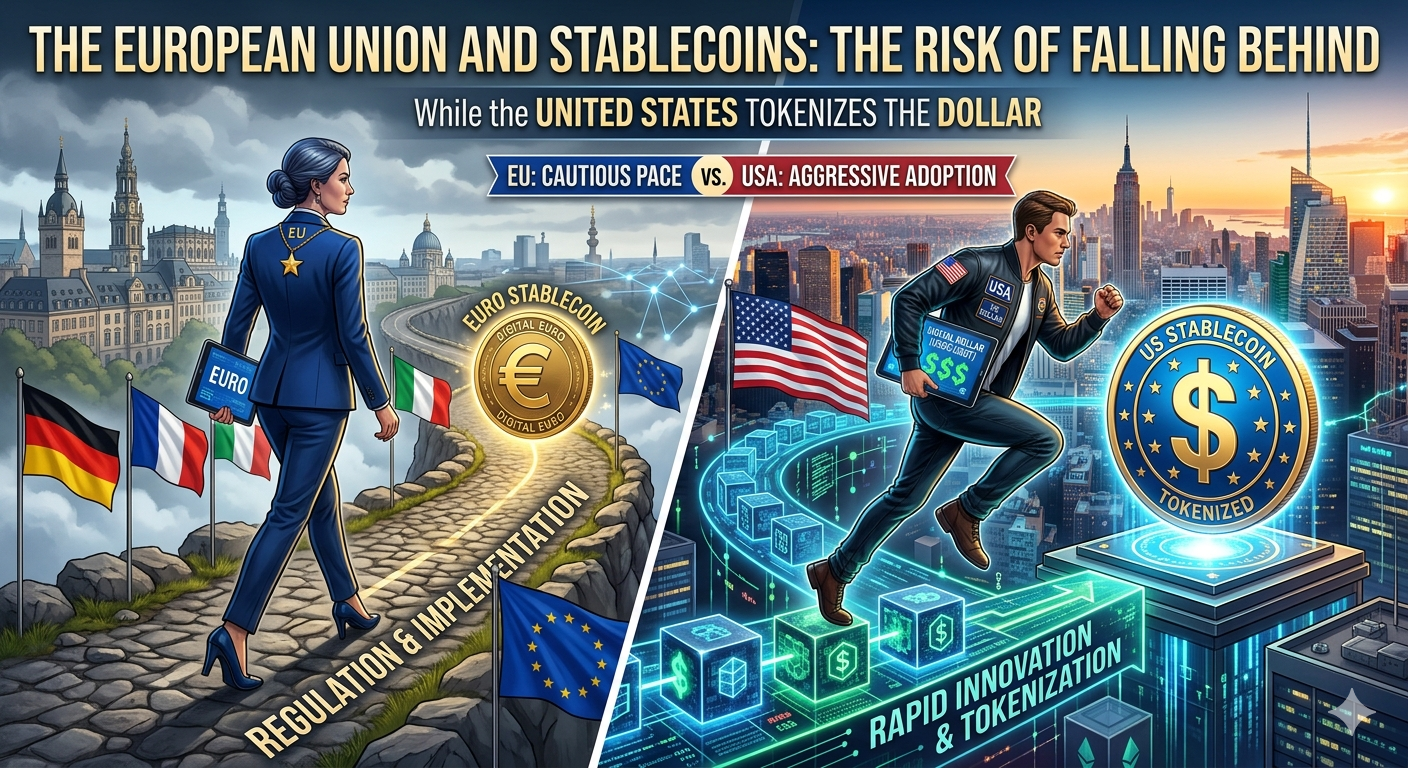

While the United States is integrating private stablecoins into its financial and monetary system, Europe continues to approach this phenomenon with a defensive logic, based on regulatory caution and the development of the digital euro as a public alternative. If this strategy is not corrected, the European Union risks being relegated within the new global monetary infrastructure.

The ECB’s Implicit Recognition

Christine Lagarde’s statements contain a relevant admission.

Stablecoins offer clear technological advantages:

- faster payments;

- lower transaction costs;

- near-instant settlement;

- programming and automation of financial flows;

- global reach without the need for traditional intermediaries.

In other words, the ECB recognizes that the technology works and that the money of the future will be digital, programmable, and interoperable with the Internet.

The issue is not technological.

The issue is who will control that infrastructure.

The United States Strategy

The United States has adopted a pragmatic and highly effective strategy.

Instead of attempting to replace the private sector with a digital currency issued directly by the Federal Reserve, it has allowed companies such as Tether and Circle to issue tokenized dollars backed by U.S. Treasury securities.

The result is extraordinary:

- international expansion of the dollar;

- structural increase in demand for U.S. public debt;

- strengthening of the American capital markets;

- consolidation of the dollar as the native currency of the Internet.

Each dollar stablecoin constitutes, in practice, a digital extension of the U.S. monetary system.

The dollar does not disappear.

It becomes tokenized.

The European Position

The European Union, by contrast, has adopted a much more restrictive approach.

MiCA has established a pioneering but demanding regulatory framework.

At the same time, the ECB is promoting the digital euro as an instrument to preserve European monetary sovereignty.

In Christine Lagarde’s words:

“Our task is not to replicate instruments developed elsewhere, but to build the foundations and infrastructure that serve our own objectives.”

The intention is legitimate. The problem is that innovation rarely waits for regulators.

While Europe designs a project whose implementation may arrive around 2029, the market is already using hundreds of billions of dollars in stablecoins for payments, savings, financing, and international settlement.

The infrastructure is already operational.

The Risk of an Excessively Defensive Reaction

Concern about “digital dollarization” is understandable.

But attempting to slow the expansion of private stablecoins without offering a competitive environment for innovation may generate counterproductive consequences.

Among them:

- relocation of projects to the United States and other jurisdictions;

- loss of talent and capital;

- lower competitiveness of the European financial system;

- technological dependence on foreign infrastructures;

- reduction of the euro’s international role.

Europe cannot protect its monetary sovereignty by limiting innovation.

Sovereignty is built by creating competitive infrastructure.

The Tokenization of Money Is Inevitable

The debate is no longer about determining whether money will be tokenized.

That transformation is already taking place.

The real question is which jurisdictions will lead the process.

The United States has understood that stablecoins are an instrument of economic and geopolitical power.

Europe still appears to view them primarily as a risk.

That approach may prove deeply costly.

The Jurisdiction of the Internet

From the perspective of Bitcoin Digital Law, stablecoins are part of a broader phenomenon: the emergence of the Jurisdiction of the Internet.

In this new sphere, money, contracts, and settlement systems are organized through coded rules and executed automatically by decentralized networks.

Whoever controls the main monetary units of this jurisdiction will hold an extraordinary structural advantage.

Today, that advantage clearly belongs to the dollar.

The Digital Euro Is Not Enough

The digital euro may play an important role.

But, by itself, it will not be enough.

Europe also needs to:

- encourage the issuance of euro-denominated stablecoins;

- simplify the regulatory framework for innovative projects;

- attract issuers and infrastructures to European territory;

- promote open and interoperable standards;

- integrate the private sector as a strategic ally.

Without a robust ecosystem of tokenized money in euros, the digital euro risks arriving late and with limited global adoption capacity.

A Strategic Decision

The European Union faces a transcendental choice.

It can continue with an essentially defensive strategy, focused on limiting risks and preserving traditional structures.

Or it can adopt an ambitious vision, recognizing that the tokenization of money represents a historic opportunity to strengthen the international role of the euro.

The United States has already chosen.

It is turning the dollar into the native currency of the Internet.

Europe must decide whether it wants to participate actively in this transformation or merely observe it from the periphery.

Conclusion

Christine Lagarde’s warning is correct in its diagnosis, but insufficient in its solution.

The real risk is not the existence of stablecoins.

The real risk is that Europe responds too late and with an excessively restrictive strategy.

If the United States successfully tokenizes the dollar and Europe fails to build a competitive ecosystem in euros, the European Union may lose influence in the new global monetary architecture.

The future of money is already being written in code.

The question is whether Europe will be an author of that code or simply a user of rules designed by others.