For decades, the global monetary system has been built on a clear institutional architecture: central banks issue money, commercial banks distribute it, and the traditional financial system acts as the universal intermediary.

However, the emergence of blockchain technology is beginning to fragment this model.

Alongside the development of Bitcoin as “digital gold” within the jurisdiction of the internet, a complementary and essential component has emerged: stablecoins. Among them, Tether (USDT) has consolidated itself as the functional equivalent of a central bank in this new digital order.

The Internet Jurisdiction and the Need for Stability

The concept of the internet jurisdiction, as developed in Ley Digital Bitcoin, is not a metaphor. It is a real normative space where rules are not enforced through state coercion, but through code and cryptographic consensus.

Within this environment, the need for a stable unit of account was inevitable.

Bitcoin fulfills the role of a store of value, but its volatility limits its use as a medium of exchange in everyday transactions. This is precisely where Tether finds its place.

USDT is not merely a dollar-pegged token. In practice, it operates as the primary liquidity layer of the crypto economy. Its scale and presence across virtually all relevant blockchains make it the backbone of digital markets.

Tether’s De Facto Central Bank Functions

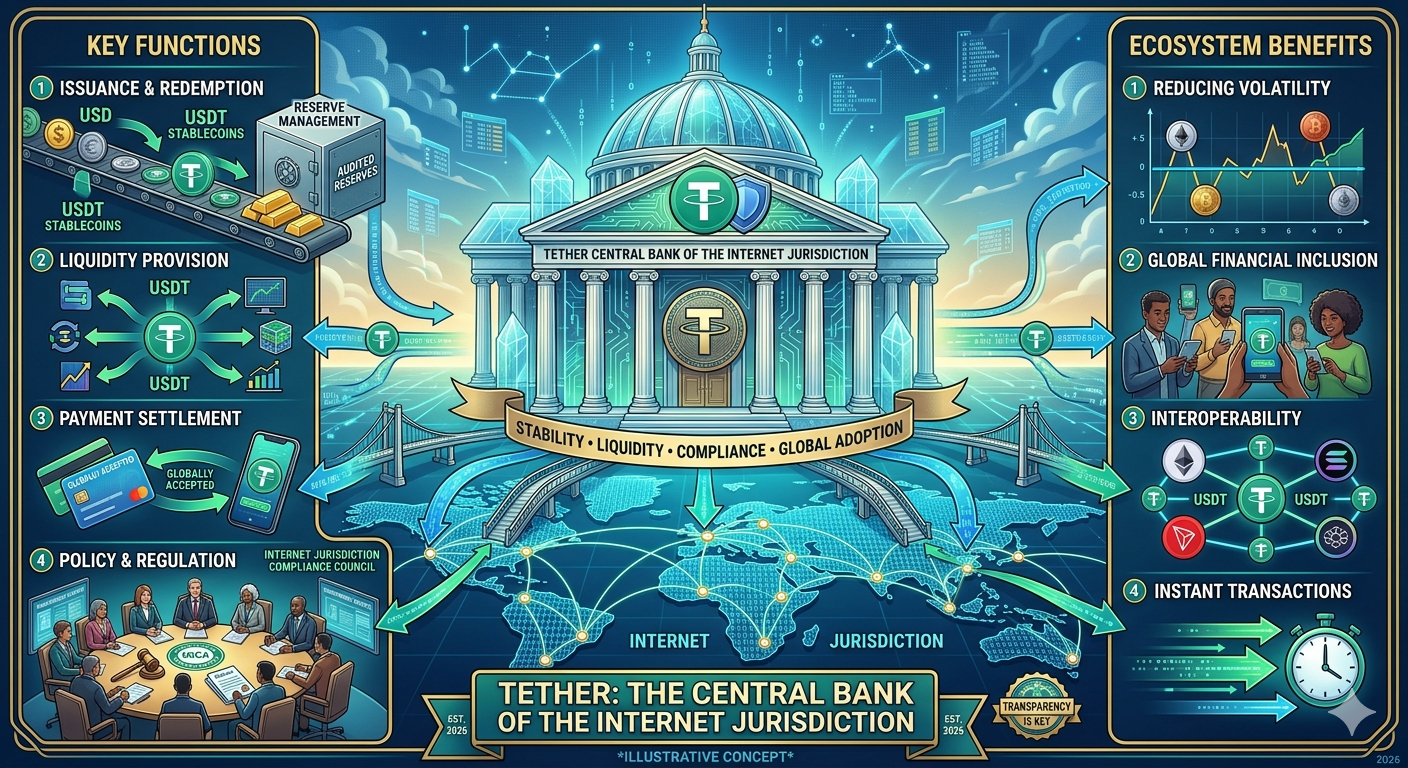

Tether’s role closely mirrors that of a central bank. In the traditional system, central banks manage liquidity, act as lenders of last resort, and provide a stable unit of account. Tether, despite lacking formal recognition, performs many of these functions within the internet jurisdiction.

1. Informal Unit of Account

Most trading pairs in the crypto ecosystem are denominated in USDT. Prices of digital assets—from Bitcoin to emerging tokens—are expressed in this stablecoin.

2. Liquidity Transmission Channel

When the crypto market expands, a significant portion of that growth is structured through the issuance of new USDT. This capacity to expand the monetary base resembles quantitative easing (QE) policies implemented by central banks.

3. Global Payment Infrastructure

In countries experiencing high inflation or capital controls, Tether functions as a substitute for the dollar. It enables near-instant, low-cost transfers without relying on banking intermediaries.

Central Bank vs. Tether: A Functional Parallel

The comparison is not merely rhetorical—it is structural:

-

- Unit of account

Central banks: national currency

Tether: USDT as crypto-denominated benchmark - Liquidity management

Central banks: monetary policy tools

Tether: issuance and redemption of tokens - Payment infrastructure

Central banks: settlement systems (e.g., TARGET2, Fedwire)

Tether: blockchain-based global transfers

- Unit of account

A Central Bank Without a State

The analogy, however, is not without tension.

Unlike institutions such as the Federal Reserve or the European Central Bank, Tether does not operate under a public mandate, nor is it subject to an equivalent regulatory framework.

Its model relies on trust in the existence and quality of its reserves—an issue that has consistently generated debate and scrutiny.

From a legal perspective, this raises a fundamental question:

Can a central bank exist without a state?

The internet jurisdiction suggests that the answer may be yes.

In this new environment, legitimacy does not derive from territorial sovereignty, but from adoption. Tether does not require state recognition to function; its authority emerges from its utility.

Legitimacy, Risk, and Lex Cryptographica

This phenomenon fits within the broader evolution toward a lex cryptographica, where rules are embedded in protocols and enforced through technical mechanisms.

In this context, Tether is not an institution in the traditional sense. It is infrastructure—part of a broader system of digital laws.

However, this reality also highlights the need for an additional legal layer.

Code can execute, but it cannot resolve all disputes.

The issuance, backing, and use of stablecoins raise complex legal questions: insolvency, fraud, contractual disputes, and regulatory compliance. This is precisely where frameworks such as BACS become relevant—introducing arbitration mechanisms capable of bridging off-chain legal enforceability with on-chain execution.

A Historical Transition

Ultimately, Tether represents a historical transition.

It is not simply a stablecoin. It is the first large-scale experiment in a monetary system operating outside the perimeter of the state, yet performing functions equivalent to those of a central bank.

Its existence demonstrates that the internet jurisdiction can create not only digital assets, but also functional institutions that replicate—and in some cases surpass—traditional structures.

If Bitcoin is the digital gold of this new jurisdiction, Tether is its dollar.

And, in practice, its central bank.