Yield has returned to the center of the crypto ecosystem, but this time under a different logic: it is not only a financial innovation, but a phenomenon in the process of regulatory integration.

The recent evolution of the criteria of the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission marks a turning point. For the first time, staking—historically located in a gray area—begins to fit within a legal framework compatible with traditional financial products, such as ETFs.

This change is not minor: it represents the transition of “crypto yield” from the regulatory periphery to the core of the financial system.

From Regulatory Vacuum to the Legal Qualification of Staking

For years, the key question has been whether staking rewards should be considered securities under U.S. law.

The dominant interpretation, based on the Howey Test, generated structural uncertainty:

Is there an investment in a common enterprise?

Do profits depend on the efforts of others?

The new regulatory approach introduces a relevant nuance: not all staking implies a traditional investment relationship. In certain cases—especially when it involves protocol validation—rewards may be considered a technical result of the network’s operation, and not a financial instrument in the strict sense.

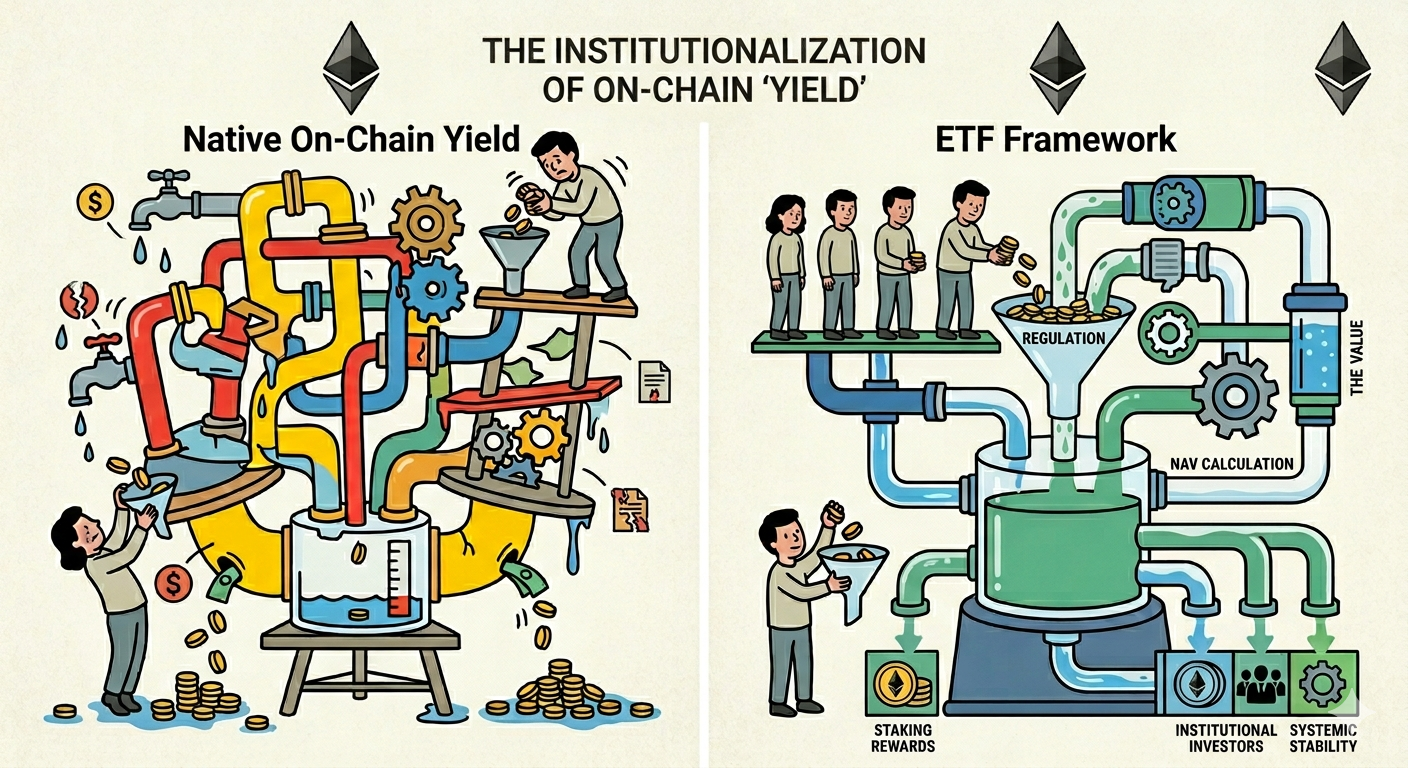

This conceptual shift enables something that was previously unfeasible: the integration of staking into regulated vehicles.

The ETF as a Bridge Between Two Legal Systems

The emergence of Ethereum ETFs with integrated staking represents a phenomenon that is more legal than merely financial.

On the one hand, these products operate within the regulated framework of the traditional securities market.

On the other, they capture yield generated in a decentralized infrastructure such as Ethereum.

The result is a hybrid that connects two normative orders:

-The traditional financial system (custody, supervision, disclosure)

-The internet jurisdiction (consensus, validation, automatic execution)

In this sense, staking ceases to be a purely technical activity and becomes a legally recognizable and structurable source of yield.

Key Actors in the Institutionalization of Staking

The entry of large asset managers has accelerated this normalization process.

Among the main players are:

-BlackRock, which has promoted products with exposure to ETH and yield-generation strategies

-Grayscale Investments, a pioneer in the distribution of structured crypto products

-VanEck, with ETF proposals that directly integrate staking

-Lido, as key infrastructure for liquid staking

These actors not only bring capital, but something more relevant: regulatory legitimacy.

Yield as an Element of Asset Qualification

From a legal perspective, the differentiating element of Ethereum compared to Bitcoin is clear: its capacity to generate yield.

While Bitcoin is configured as a passive asset (store of value), Ethereum introduces a productive dimension.

This has direct implications for its qualification:

-The asset ceases to be merely speculative

-It approaches traditional categories such as income-generating assets

-It allows its integration into institutional portfolios under risk-adjusted return criteria

The data is significant: ETH ETFs with staking offer an estimated net annual yield of 2–3%, compared to the structural 0% of spot Bitcoin ETFs.

Regulatory Risks and Structural Tensions

However, this institutionalization is not without legal and operational risks.

- Liquidity Risk

Staking implies a temporary lock-up of assets. In an ETF, this creates a structural tension:

The investor demands immediate liquidity

The protocol imposes exit times

This mismatch may force managers to operate in secondary markets, introducing price and execution risks.

- Regulatory Requalification Risk

The current criteria of the SEC and the CFTC are not necessarily final.

A change in interpretation could:

Reclassify certain staking structures as securities

Impose additional obligations on issuers and managers

Directly affect the viability of ETFs

- Concentration Risk

The use of protocols such as Lido introduces a critical issue: the centralization of validation within infrastructures that are apparently decentralized.

From a legal perspective, this reopens the debate on:

-Liability

-Governance

-Possible qualification as an intermediary

Implications for Future Regulation

The development of ETFs with staking forces regulators to address a structural question: how to integrate yield sources native to blockchain within frameworks designed for traditional financial instruments.

In Europe, the Markets in Crypto-Assets Regulation does not yet fully resolve this issue.

This opens several scenarios:

-Development of specific regulation for staking

-Adaptation of existing categories (CASP, custody, management)

-Creation of hybrid standards between financial law and blockchain architecture

Conclusion: From Technical Yield to Legal Yield

The real change is not that Ethereum generates yield.

The change is that this yield is beginning to be recognized, structured, and distributed within traditional legal frameworks.

This marks the beginning of a new phase:

-Staking ceases to be a technical activity

-It becomes a relevant legal category

-And it becomes part of the global financial system

Ultimately, Ethereum ETFs with staking are not just investment products.

They are the first clear manifestation of how the internet jurisdiction begins to integrate—and tension—traditional financial law.