For a long time, stablecoins have been presented as a simple technological innovation: digital tokens whose value remains stable because they are backed by fiat currencies, mainly the United States dollar.

However, this description is insufficient.

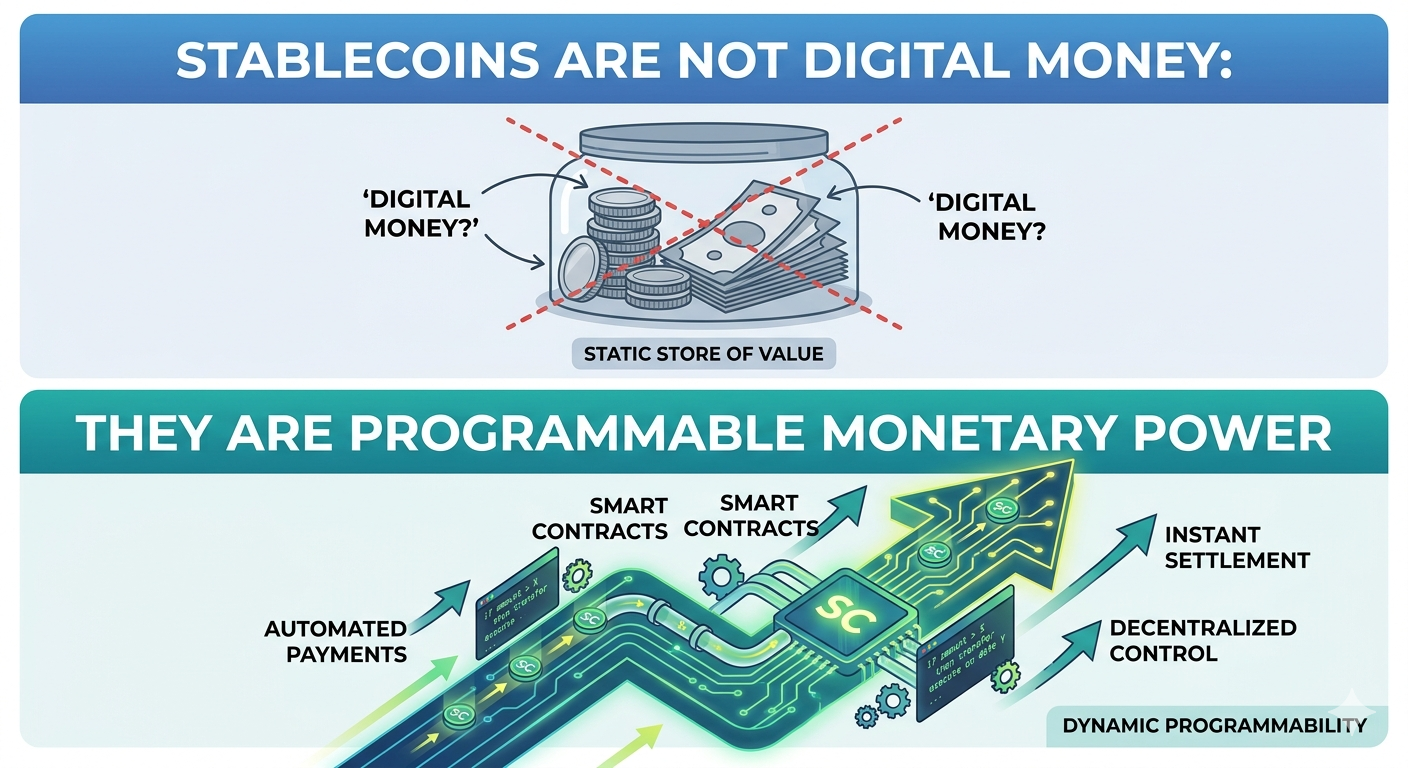

Stablecoins are not merely digital money.

They are a new form of programmable monetary power.

And that difference is fundamental.

From Money to Code

Money has always been a legal and political institution.

A banknote is not valuable because of the paper from which it is made, but because there is a legal and institutional structure that guarantees its acceptance, its convertibility, and its use as a means of payment.

In the traditional system, monetary issuance has historically been reserved to States and central banks.

With the emergence of Bitcoin, a decentralized monetary system capable of functioning without a central authority appeared for the first time.

Later, Ethereum made it possible to create programmable tokens and smart contracts.

On that infrastructure, a new phenomenon was born: stablecoins.

What Is a Stablecoin Really?

A stablecoin is a digital token designed to maintain a stable value, normally equivalent to one United States dollar.

Well-known examples include Tether, USD Coin, and Dai.

At first glance, they appear to be simple digital representations of the dollar.

But their nature is much deeper.

A stablecoin combines three elements:

- A monetary unit.

- A globally transferable digital asset.

- A set of programmable rules executed automatically.

Consequently, we are not dealing with passive digital money, but with money that has behavior built into it.

The Birth of the Private Digital Dollar

For decades, the dollar existed in two main forms:

- cash issued by the Federal Reserve;

- bank deposits held within the financial system.

Stablecoins introduce a third form:

the Internet-native digital dollar.

This dollar can circulate 24 hours a day, settle in seconds, and be used in global financial applications without the need for correspondent banks.

For this reason, stablecoins constitute the most advanced version of the international dollar.

They do not depend on borders, banking hours, or traditional intermediaries.

They function as a global monetary infrastructure.

Programmable Monetary Power

The true innovation does not lie only in the digitization of the dollar.

The innovation is that money can incorporate automatic rules.

A stablecoin can:

- be blocked;

- be frozen;

- be transferred automatically;

- generate yield;

- serve as collateral;

- be integrated with lending protocols;

- distribute payments to artificial intelligence agents;

- execute according to predefined conditions.

In other words, money ceases to be a static instrument and becomes software.

And whoever controls that software controls a form of monetary power.

Tether and the New Private Central Banks

The case of Tether Holdings Limited is paradigmatic.

Tether issues tens of billions of digital dollars and maintains a substantial part of its reserves in United States Treasury securities.

In practice, Tether performs functions typical of a private monetary authority:

- it issues monetary units;

- it manages reserves;

- it manages liquidity;

- it facilitates global payments;

- it can freeze assets.

Without being a formal central bank, it operates as one within the jurisdiction of the Internet.

This demonstrates that monetary power no longer belongs exclusively to States.

The GENIUS Act and the Integration of the Digital Dollar

In United States, the legislative debate on stablecoins has crystallized in proposals such as the GENIUS Act.

The underlying philosophy is clear: to allow private issuers to operate under supervision, provided that they maintain secure reserves, mainly in Treasury securities and cash.

The strategic objective is to consolidate global demand for United States public debt and reinforce the hegemony of the dollar.

In this context, stablecoins become a geopolitical instrument.

Each token backed by dollars increases the monetary influence of the United States over the global digital economy.

Europe and the Risk of Irrelevance

The European Union has responded through Markets in Crypto-Assets Regulation (MiCA), which establishes a legal framework for issuers and crypto-asset service providers.

Although MiCA provides legal certainty, the European approach remains primarily defensive.

While the United States uses stablecoins to expand the digital dollar, Europe focuses on limiting risks and on developing the digital euro.

The result may be a growing dependence on dollar-denominated monetary infrastructures.

Stablecoins and the Agent Economy

The next major transformation will be the integration of stablecoins with artificial intelligence agents.

An autonomous agent will be able to:

- contract services;

- pay for computing resources;

- receive income;

- invest surplus funds;

- execute automatic agreements.

All of this using stablecoins as a means of exchange.

In this scenario, programmable money will be the operational foundation of the automated economy.

It will not merely be about faster payments.

It will be about economic systems that function autonomously.

The Legal Dimension

If stablecoins represent programmable monetary power, their regulation cannot be limited to technical or prudential issues.

It must address essential questions:

- who may issue digital money;

- what rights users have;

- in which cases funds may be frozen;

- which jurisdiction resolves disputes;

- how decisions are enforced.

This is where institutions such as BACS become relevant, conceived to provide arbitration and legal enforcement within blockchain infrastructure.

Because programmable money also requires programmable justice.

Conclusion

Stablecoins are not simple digital versions of traditional money.

They are a new monetary architecture.

They transform the dollar into software.

They turn currency into a global infrastructure.

And they transfer part of monetary power from central banks to private issuers and technological protocols.

Ultimately, stablecoins are not merely digital money.

They are programmable monetary power.

And whoever controls that infrastructure will control an essential part of the Internet economy.